Gas stations are unique properties that can be sold as fee simple, leased fee, or leasehold estates. Operating fee simple gas station sales include the assembling of real estate, personal property, and business assets, often referred to as the “going-concern.” Leased fee sales occur when landlords sell real estate encumbered by a lease, while leasehold sales happen when tenants sell a business encumbered by a lease. This article focuses on operating fee simple gas stations selling on a going-concern basis to include:

- Real Estate (land, buildings, fueling improvements, and permanently attached equipment or fixtures)

- Personal Property (removable equipment, furniture, tools, and non-permanent assets that can be removed without damaging the remaining real estate)

- Business (intangible assets, vendor agreements, assembled workforce, fuel supply, branding, etc.)

The Uniform Standards of Professional Appraisal Practice (USPAP) require appraisers to allocate real estate, personal property, and business (intangibles) assets in going-concern appraisals. Various allocation methods exist in the market, let’s first examine how fee simple gas stations are generally valued.

Valuation techniques suitable for general commercial real estate may not be appropriate for fee simple gas station going-concerns. Fee simple real estate is typically valued using the Sales Comparison Approach based on price per square foot. Comparable sales are gathered, prices per square foot are adjusted, and market value is determined. While this methodology may be credible for general real estate valuation, it can be misleading when applied to fee simple gas stations that include personal property and business assets in addition to real estate.

Because the operating business cannot be relocated or sold separately without a lease in place, the fee simple gas station business is assembled with real estate and personal property creating the going-concern. This necessitates specialized valuation techniques to value these assets as assembled in bulk and not sold separately.

To arrive at fee simple market value for the going-concern including real estate, personal property and the business we apply an income multiplier to gross profits or EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). For example, a gas station with $1,000,000 in gross profits may be worth $5,000,000 as a fee simple going-concern using a 5.00 Gross Profit Multiplier (GPM):

$1,000,000 Gross Profit x 5.00 GPM = $5,000,000

Valuing the going-concern in its entirety is relatively straightforward. However, appraisers following USPAP must allocate the $5,000,000 going-concern value to real estate, business, and personal property. The allocation of business assets is a particular concern, as there are no “rules of thumb,” standard dollar amounts, or ratios to aid in business allocation. Each gas station differs in terms of real property assets, age, condition, branding, location, building size, land area, and more.

Over the past decade, gas station businesses have experienced significant changes in their cash flow performance, primarily due to higher fuel margins following the COVID-19 pandemic. Operators realized they could achieve greater profits by selling less fuel at exponentially higher margins. This trend has continued and is now the accepted strategy. As a result, fueling profits have increased, with most stations generating significantly greater cash flow than before the pandemic.

This strategy shift and value increase has widened the gap between business and real property allocations. As prices paid for gas stations are a multiple of earnings, significant increases in cash flow result in significant increases in going-concern value. However, these increases may not be spread equally between business and real estate. Gas stations have a significant portion of their real estate value in the fueling station, which consists of short-lived assets. While land tends to appreciate, buildings and the fueling station depreciate, offsetting each another. The real estate portion of a going concern tends to be more stable over time while the business is more volatile. When gas station values spiked over the past few years, the going-concern value increase was primarily in business assets, not real estate. This further widened the gap between real estate and business allocations making financing of sales more difficult. Banks prefer to lend on real estate not business or intangible assets. Buyers are motivated to the highest real estate allocations they can achieve.

RPC clients often inquire about obtaining new real estate loans knowing the value of their fee simple gas station going-concern may have doubled since their last loan. They want to capitalize on the increase and take cash out for other investments or renovations. These borrowers often assume if their fee simple going-concern value doubled so did their real estate value or allocation. Unfortunately, this is not the case, as recent value increases are primarily attributed to business assets, not necessarily real estate. If a gas station going-concern doubled its cash flow overnight, the market might pay twice as much, but the increase in value would be attributed to the business, not real estate.

The accepted methodology for allocating business value involves employing a residual technique, achieved by deducting the Cost Approach or landlord assets (Real Estate and Personal Property) from the fee simple going-concern value. For example, deducting a Cost Approach of $3,000,000 from the $5,000,000 going-concern value would leave $2,000,000 to the business. If the Cost Approach exceeds the going-concern value, there is no business allocation, with the negative difference identified as functional and/or external obsolescence.

Buyers are required to allocate the going-concern sale price between business, personal property and real estate for tax assessment purposes. However, they are not required to make these allocations based on “market” and tend to allocate in a way that benefits themselves. A higher allocation to real estate results in reduced financing costs and increased depreciation on the books.

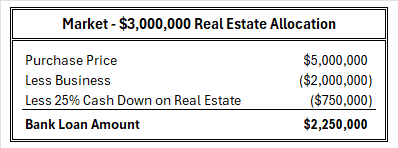

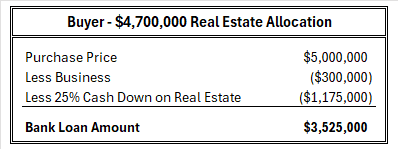

Conventional banks tend to finance real estate only. Assuming a $5,000,000 going-concern purchase and 75% loan to value ratio for real estate financing, a real estate allocation of $3,000,000 requires $750,000 cash down (a loan amount of $2,250,000). Compare this to a real estate allocation of $4,700,000 that requires $1,175,000 cash down (a loan amount of $3,525,000). We can easily see why buyers skew their allocations in favor of real estate. Depreciation benefits further support above-market real estate allocation.

The above example illustrates a difference of well over a million dollars in loan funds, significantly affecting cash-on-cash returns, especially when interest rates are favorable to the buyer. Buyers are motivated to allocate as much as possible to real estate, while ethical gas station specialists allocate based on market-supported techniques like the Cost Approach.

Assessors recording the going-concern sales of gas stations report the real estate allocation made by buyer as the “sale price”. Business and personal property assets are excluded from the roll. The Assessor tends not to challenge buyer-made allocations resulting in excessive real estate assessments that are often successfully challenged and reduced years later through the tax appeal process. Gas station appraisers understand that the “sale price” used by assessors represents the real estate allocation per buyer, not the total going-concern price. Obtaining the true going-concern sale price is challenging as parties to the transfer generally sign Non-Disclosure Agreements (NDAs). Going-concern sale prices are not generally available to the public, and there are no reliable sources for this data. As RPC appraises hundreds of gas stations each year, we are uniquely qualified, having access to true going-concern sales rather than relying on skewed real estate allocations found on the assessor’s roll and Costar’s data base.

Costar, the world’s largest commercial database of comparable sales, is the “go-to” source for “comps” used by most commercial real estate appraisers. RPC subscribes to Costar but not for the sale of going-concern gas stations. Costar users believe they are using verified real estate sales when, in fact, they are using a buyer’s inflated allocation to real estate and not the true going-concern sale price. As stated going-concern sales are highly confidential unless you are a party to the transaction (buyer, seller, broker, or appraiser).

RPC commonly reviews appraisal reports from firms not specializing in gas stations that use Costar data and price per square foot analysis for fee simple gas station valuation. Banks lend on real estate and often ask appraisers to value real estate only, ignoring business and personal property. Generalist appraisers claim competency since they are valuing real estate and not business or personal property. USPAP caution appraisers from valuing a component of the going-concern without identifying all components and how their allocation may affect one another. Fee simple operating gas stations are special-use properties where the business cannot be relocated or severed from the real estate. USPAP advises against providing real estate only market value as a portion of a going-concern.

In summary, generalist appraisers’ use of Costar gas station comps often results in overvaluing the real estate and ignoring business and personal property, a potential USPAP violation. A significant number of gas station appraisals are performed by generalists rather than gas station specialists. Bankers, assessors, brokers, appraisers, and others relying on Costar data should exercise caution. Banks may think they are protected but often underwrite real estate that is exaggerated.

It should also be noted that the allocation of real estate as part of a going-concern does not imply market value for real estate by itself. Real estate cannot be sold separately or isolated from the business unless the gas station is closed with no operating business, or the real estate is leased. Appraising a closed or leased fee gas station would yield different appraisal results than the same real estate allocated as a portion of a operating gas station fee simple going-concern.